In my previous post on Capital Gain Tax – Short Term Capital Gain we discussed capital gain tax in detail. We also discussed how short term capital gain tax is calculated. Before going through this post, I would request you to go through my previous post. This post is continuation of previous post Capital Gain Tax – Short Term Capital Gain. In this post we will discuss Long Term Capital Gain and why it is so critical from Income Tax Perspective. Just to recap, If the capital asset is held by an individual for a period more than min Holding Period as specified for each capital asset then Gain / Loss from such capital asset is termed as Long Term Capital Gain. To understand the concept of Long Term Capital Gain, first we will discuss Inflation and Inflation Indexation.

Inflation

As per Wikipedia, Inflation is a sustained increase in the general price level of goods and services in the economy over a period of time. In layman terms, if a particular set of goods and services cost Rs 100 during FY 2013-14 and inflation is 10% then same goods and services will cost Rs 110 in FY 2014-15. In short, Inflation reduces purchasing power of money and eats into your returns. In most of the articles you must have read that Returns should beat Inflation so that Real Returns are positive. Now assume, you invested Rs 100 in FD and post taxation your return is 6.3% therefore after 1 year your 100 Rs will be Rs 106.3. But with 10% inflation, now you need 110 Rs to buy same goods and services therefore your Real Return from Investment is Negative i.e. Rs 106.3 – Rs 110 = -3.7 Rs or – 3.7%. If Return on Investment is 10% then your Real Return is Zero as you have just beaten inflation.

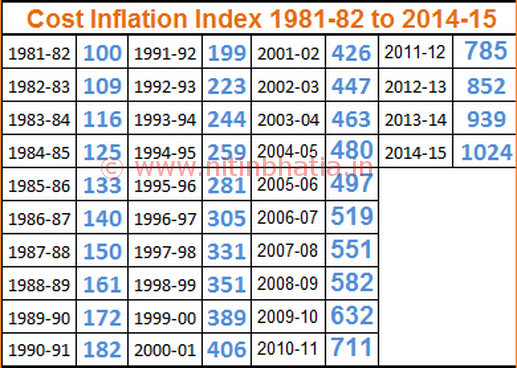

Inflation Indexation

Inflation Indexation takes care of Impact of Inflation during the Investment period. In layman terms, Inflation Indexation helps to calculate indexed cost i.e. inflation adjusted purchase price / cost of any capital asset. For every Financial Year, Govt of India declare Cost Inflation Index (CII) value for taxation purpose. Latest cost inflation index is as follows

With the help of Cost Inflation Index, we can calculate Indexed Cost using following formula

Purchase Price of a Capital Asset X Cost Inflation Index Value of FY of Sale

Indexed Cost = ______________________________________________________

Cost Inflation Index Value of FY of Purchase

For Example:

Purchase Price of a Capital Asset = Rs 40,00,000

FY of Purchase: 2010-11

Cost Inflation Index Value of FY of Purchase = 711

FY of Sale: 2014-15

Cost Inflation Index Value of FY of Sale = 1024

40,00,000 X 1024

Indexed Cost = ________________ = Rs 57,60,900

711

How Long Term Capital Gain is Calculated?

Long Term Capital Gain can be calculated by subtracting Indexed Cost of a Capital Asset from Sale Price. In above mentioned Example, if you bought a property worth 40 lakhs in Oct, 2010 and sold it for 60 lakhs in Oct, 2014. Since holding period is more than 3 years therefore Long Term Capital Gain will be 60 lakhs – 57.60 lakhs (Indexed Cost) = 2.40 lakh. In case of a property, cost of improvement & cost of transfer can also be included in the cost of acquisition for long term capital gain tax calculation. Long Term Capital Gain from Property is a complex subject, i will discuss it in detail in my future post.

Important points related to Long Term Capital Gain / Loss.

(a) Long Term Capital Loss can only be offset against Long Term Capital Gain.

(b) Long Term Capital Loss from Stocks or Equity Funds cannot offset if Security Transaction Tax is paid (Long Term Capital Gain is Tax Free).

(c) Long Term Capital Loss cannot be offset against Income.

(d) Long Term Capital Gain can be offset against Short Term Capital Loss.

(e) Any loss from business or profession can be offset against Long Term Capital Gain. Similar to Short Term Capital Gain, Any carry forwarded business losses cannot be set off against long term capital gain.

Long Term Capital Gain Tax Rate

(a) Stocks and Equity Oriented Funds: NIL (Fully Exempted)

(b) Bonds and NCD’s (Non Convertible Debentures): 10% Flat without indexation benefit

(c) Debt Oriented Funds: 20% with indexation benefit

(d) Gold ETF’s and Gold Funds: 20% with indexation benefit

(e) Bullion and Jewellery: 20% with indexation benefit

(f) Real Estate: 20% with indexation benefit

Therefore if Long Term Capital Gain is 2.4 Lakh (as calculated above) with indexation benefit, Tax rate is 20% (irrespective of the tax slab of the investor). Long Term Capital Gain Tax will be 20% of 2.4 Lakh = Rs 48,000.

Imp Point: Tax rate of Long Term Capital Gain is independent of Tax slab of the investor. Some of my readers who were in 10% income tax slab took indexation benefit but considered tax rate at 10% (individual income tax slab) instead of 20%. With Indexation benefit, Long Term Capital Gain Tax rate is 20%.

If you are an ACTIVE investor in stock market then you might need to pay Long Term Capital Gain Tax as per your Income Tax slab without indexation benefits as Income tax department might treat your stock activity as Business Activity. You will be taxed as per your income tax slab.

Smart Investor

Lastly a smart tip on how to gain maximum from inflation indexation. If you are planning to invest in debt market or real estate for 3 years or more then it is advisable to invest towards the end of Financial Year i.e. during February or March. After 3 years, You can sell your capital asset at the beginning of Financial Year i.e. in April or May to avail indexation benefit of new FY. Through this strategy, you can avail inflation indexation benefit of 4 Financial Years by investing only for slightly more than 3 years. Lets understand with an example.

Assuming, i bough debt mutual funds worth Rs 1 lakh on 20th March, 2012. My minimum holding period of 36 months will be over on 19th March, 2015 and if i sell after this date then any gain will be long term capital gain. I can avail indexation benefit. Now if i wait for 2 more weeks and sell my mutual funds on 5th April, 2015 then Cost inflation index value of FY 2015-16 will be considered instead of FY 2014-15. Average inflation during current FY i.e. 2014-15 is 8% and assuming Cost Inflation Index value of 1105 for FY 2015-16 based on inflation. In short, by deferring my redemption for few days the indexed cost will be high thus my long term capital gain will be less. This strategy works only when Inflation is high.

Indexed Acquisition Cost (Redemption on Mar 20, 2015): Rs 1,30,445

Indexed Acquisition Cost (Redemption on April 05, 2014): Rs 1,40,764

Irrespective of NAV at the time of Redemption, by deferring redemption my long term capital gain will reduce by approx Rs 10,319. If we assume that NAV will remain almost same (NAV of debt mutual fund is not very volatile) then i can save Rs 2063 as Long Term Capital Gain tax with this smart strategy.

This conclude, one of the most interesting topic of Personal Finance / Taxation. Hope you liked the post. You can share this post with your friends and family members through following social media icons. For any query / clarification, Please feel free to leave your comments in following comments section.

Copyright © Nitin Bhatia. All Rights Reserved.

Hello Sir, can the long term capital gain can be used to pay off another home loan?

You can do that but it depends on case to case basis i.e. when other property is bought. In short, this property should be eligible to set off long term capital gain.

Request please explain the time available to invest in “Capital Gains Tax Exemption Bonds or 54 EC bond ” to claim tax exemption. Suppose I sold a property on 10th June 2015 and I want to claim tax exemption by investing in these bonds . Please advise the time available with me to invest in these bonds and claim exemption.

Sameer Vip

6 months from the date of sale.

Hi Sir, I bought a property from NRI for 50+ lakhs. The seller asked me to Not to deduce TDS and gave me an affidavit stating “no TDS should be deduced,as seller would be taking care of Tax implications and file the IT returns”. I did not deduce any TDS. I received a 26 QB notice from IT department. Would you please let me know what I should do in this case ?

TDS is responsibility of a buyer. In case of NRI, TDS should be u/s 195. It seems IT department is not aware that seller is NRI. You have to bear all penalties and pay TDS amount. Please check my posts on TDS if the seller is NRI.

Hi Nitin,

Very nice post. I read your post regularly

I have a question for you.I invested in equity mutual fund (ELSS) few years before and is thinking of redeeming the same before 10 years. I understand since it is long term CG (>1 year) , tax is not there but I need to declare it in ITR -2 . Is my understanding correct ? Also where in ITR-2 do I need to declare it under capital gains or under exempt income for which STT was paid ?

Thanks

There are 2 thoughts on same (a) As there is no Long Term Capital Gain Tax therefore no need to declare (b) Though Long Term Capital Gain Tax is Nil but Long Term Capital Gain is booked therefore it should be declared in ITR-2. There is no clarity and consensus on this. Hope we will have clarity in next FY’s budget.

Thank you Nitin …

Hello Sir, For tax of sale of property, I agree that from April 1’st 2015 the tax on LTCG is flat 20% with indexation benefit. But if I sell property before April 1’st 2015 can I avail LTCG at 10% without indexation? (as per my knowledge this has been removed only in this year budget).

Thanks.

sham

The provision shared by you is already removed. You cannot pay LTCG tax at 10% without indexation.

Hello Sir, While calculating capital gain on property sale (Flat), Can i consider the cost of improvements for only one period or multiple periods (ex: in 2005-06, 2009-10, 2014-15). etc. then calculate the indexed cost and total the same. Also wanted to know if any furnishing done and is sold to the new buyer can be considered in cost of improvement ?

You can consider any no of periods. Furnishing is not included in the cost of improvement.

Nitin Ji What is CII rate for FY 2015-16

It is not declared yet due to long holidays during this week. It is expected any time soon.

Nitin Ji what happens if a plot was booked in 2007, installments were paid till 2011 when it was registered in my name and it is sold in 2015-16? Would the Index be applied to each installment individually or on the total amount paid till 2011, when the plot was registered in my name.

You have not mentioned when you received allotment letter from the builder.

June 2007 I got my Allotment letter. But I had made major payments by then. Out of total of 14.92 lacs, I had already paid some 11.76 lacs before June 2007.

Date of issue of allotment letter is considered as Date of Acquisition.

Sir Waiting for reply!

Please have patience. All queries are answered within 2-3 days. The query was posted less than 24 hours.

I calculated long term capital gains for sale of property and your post was very useful. Iam planning to invest in capital gains bond. Capital gain is Rs.1575168, can I invest in bonds for 16L?

Capital Gain Bonds are available in denomination of Rs 10000 therefore you can buy 158 bonds of Rs 10000 each.

Thankyou Sir. How should I show the sale of the property in income tax since Iam a tax payer? After getting capital gains bond, where should it be mentioned in income tax?

You need to file ITR 2. There is a section for capital gain.

Thanks Sir. I would like to know whether ITR 2 can be filed online. Thanks in advance

Yes, you can file ITR 2 online.

Nitinji, I booked a flat in yr 2009 and availed a home loan to pay the installments. On paying the booking amount the flat was allotted to me. Due to the recent judgement of NGT, the flat can not be registered in my name and I have not got possession from the builder, I wish to sell the under construction flat. Will I be charged LTCG tax on the profit made on sale proceeds? or STCG tax? or no tax will be levied at all as technically speaking I have not yet acquired the flat. Thanks in advance.

You need to pay LTCG tax on the sale of property.

Hello Nitinji.

I found your posts on various financial matters very pragmatic and all views are precise with clarity. As a continuation of the discussion on capital gains and tax related to it, can you throw some light on technicalities involved in investment of the either the total sale proceeds or only gains part of the transaction under section 54EC and 54F of Income tax act.

You only need to invest capital gain not total sale proceeds.

would like to know the CBDT declaration of cost inflation index for assessment year 2016-17 (financial year 2015-16)

It is not declared yet.

Sir Is the interest from capital gains bond taxable?

Interest received from capital gains bonds is fully taxable under the head “Income from other sources”.

Thank you Sir.

for purchase of under construction flat which date is considered as purchase date, allotment date, registration date, oc date or possession date. Need to know this for calculating LTCG

for purchase of under construction flat which date is considered as purchase date, allotment date, registration date, oc date or possession date. Need to know this for calculating LTCG

Date of Allotment.

Hi Nitin ji, I have 2 questions a) which year is considered as year of purchase – Agreement to buy or stamp duty/registration b) Whether Indexed cost may also include the yearly property tax and society maintenance charges

1. Agreement to buy

2. No

Hi Nitinji,

One of my friend booked a flat in 2005 by cheque payment and the property was registered in 2010 after 100 % payment. Builder never gave the possession letter and the sale deed was cancelled a couple of months back. Builder has paid the amount paid for the flat + some amount as compensation and interest. Cancellation deed only mentions payment of one DD (which is equivalent to the amount paid to builder in 2010). Compensation amount is not mentioned in the cancellation deed.

Does this qualify for capital gain?

You have not mentioned how the compensation + interest is paid to your friend by the builder.

Entire amount has been paid in 4 different Pay Orders.

1. Original amount

2. Interest

3. Compensation

4. To settle all the disputes

You need to pay capital gain tax on compensation amount.

hello mr bhatia,

i want to understand the long term capital gain with dividend reinvestment option. will you help me understand. say for eg, 1000 shares bought for 1000, and then same fy 20% dividend which is reinvestment and then after 3 years it was sold at a profit, how do we treat the dividend reinvestment option with the long term capital gain calculation…

Dividend Reinvestment is considered as fresh Investment only. As you sold after 3 years therefore Long Term Capital Gain Tax is not applicable. Enjoy the profits :)

Hello Mr. Nitinji. thanks for your good guidance. I need guidance regarding . That If suppose i have started SIP of Rs. 1000 on january , 2000 & till may 2015 I will continue. And now suppose i want to withdraw money 13,00,000 around at investment of around 1,85,000. then what tax rate is applicable & how it will be apply. If long term capital gain then the 13,00,000 income would be count in income from other source.

Your query is not clear. You mentioned that you would like to withdraw 13 lakh. Please let me know in which type of mutual fund or stocks you would like to invest and what appreciation rate is considered by you.

Hi Nitin,

I have a query, if we register a plot on govt value say (7 lac) and sale agreement value (15 lac). which value we need to consider for the capital gain? if 7 lac then whats about remaining 8 lakh? can we consider the sale agreement cost while computing the capital gain. or apart from sale agreement do we need to sign on DOTOR which you mentioned in other post?

Please clarify on this

Sale agreement value i.e. 15 lac for calculation of capital gain.

Thanks Nitin Ji.

So we can go ahead and register for govt guidance value.

Do we need to sign on DOTOR doc for fill the gap of sale agreement – registration value. Because on sale agreement build has divided the total price between land cost + development cost.

I can answer only after going through your documents.

Hi Nitin.

Wanted to know by when can we expect the Cost Inflation Index to be announced for FY 2015-16 ? And as per your estimates what should be the approximate figure ?

It is not yet notified by the Govt of India. It is difficult to estimate. I suggest you to wait for official communication.

Please advise your opinion in the following matter of LTCG.

A plot was purchased by a person in 2012-13 (March 2013) at a registered cost of Rs.52500. A house was constructed in FY 2013-14 with a bank loan of Rs.3,75,000/-. The said loan was fully paid by 2011-12. Improvement (extension of 1st and 2nd floors) was completed in FY 2013-14 at a cost of Rs.17.00 lakhs by obtaining bank loan. Supposing that the entire property (consisting of Ground, First and Second Floors) was sold in FY 2015-16, i.e for an agreed price of Rs.66.00 lakhs (registered cost of Rs.27.80 lakhs) what will be the effect of it?.

– Whether it will be LTCG or STCG?

– How to deal with the differential amount?

– What would be your sincere advise in this regard in so far as Capital Gain taxation is concerned, including advance tax payment if any?

This forum is only for general discussions. For any personalized consultation, you may opt for paid services.

Hello Nitin Ji,

I booked a flat in 2010 with my wife as co-applicant. The builder buyer agreement was signed on 16th Aug’10 and the allotment letter was issued by builder on 29th Aug’10. I sold the under construction flat in Jul’14 and bought another flat in Aug’14 with my wife again as a co-applicant.

Will both of us be required to show the LTCG in income tax return and file ITR-2 or only I need to show it as I am the main owner/applicant. Further, will year 2010-11(year of allotment) be taken for indexation to determine the cost of acquisition or the years in which each of the instalment was made will be taken as indexation for that particular instalment.

Kindly clarify.

LTCG will be in proportion of ownership in the property. For indexation, you may consider FY 2010-11.

Thanks for your prompt reply Nitin Ji,,

After sale of under construction flat, we paid 45 lac for new property and 5 lac balance amount is to be paid later. Now while filing ITR, what amount each of us (me and my wife) should mention as “Cost of New Asset”- 22.5 Lac or 25 Lac. Please suggest. The LTCG was only 6 lac and that has already been reinvested as part of 45 lac paid amount.

Without calculations i cannot comment

Hello Nitin ji,

I bought a Flat through Bank loan. Is the Bank Interest paid will also be considered to arrive at purchase cost of the Flat. And whether LTCG exemption is available if I have two properties and I intend to sell one of them.

Home Loan Interest cannot be included in property cost. LTCG for each property is calculated separately subject to certain conditions.

Sir,

I sold my under construction flat after holding it for more than three years from date of allotment and paid interest on my bank loan during this period. As possession of the flat was not offered to me and I have not claimed any tax benefit on interest amount paid to bank, shouldn’t the bank interest paid be included in cost of acquisition with proper indexation.

You cannot include interest in cost of property acquisition.

Sir,

I am selling my property and for calculation of index cost I am bit confused about the year to be considered for index rate. As I have made part payment in F.Y 2003-04 and part in F.Y 2004-05.

Please help which F.Y I need toconsider for calculation of index ation cost ??

Consider FY in which you received Allotment Letter.

YESTERDAY

CA Akhilender Singh

7:28 AM

+91 99 90 057390CA Atul Agrawal

[7/23/2015, 9:56 PM] +91 99 90 057390: CIC directs bank to provide information as to under what regulations loan applicants are required to get their project reports certified by CA

Central Information Commission New Delhi vide order dated 19-06-2015 has directed Central Public Information Officer(CPIO),Bank of India to forward to the Appellant a certified copy of the bank regulations / guidelines, which require loan applicants to submit their project reports and project balance sheets certified by a Chartered Accountant.

In case there are no such specific regulations / guidelines, the CPIO should inform the Appellant accordingly in writing. The CPIO to comply with above directives within fifteen days of the receipt of order, under intimation to the Central Information Commission

9:56 PM

+91 78 27 037060 CA Raghav Garg

[7/23/2015, 9:59 PM] +91 78 27 037060:

9:59 PM

+91 98 10 502399CA.Manoj Sangal

[7/23/2015, 10:18 PM] +91 98 10 502399: Nice Story

अमेरिका की बात हैं. एक युवक को व्यापार में बहुत नुकसान उठाना पड़ा.

उसपर बहुत कर्ज चढ़ गया, तमाम जमीन जायदाद गिरवी रखना पड़ी . दोस्तों ने भी मुंह फेर लिया,

जाहिर हैं वह बहुत हताश था. कही से कोई राह नहीं सूझ रही थी.

आशा की कोई किरण दिखाई न देती थी.

एक दिन वह एक park में बैठा अपनी परिस्थितियो पर चिंता कर रहा था.

तभी एक बुजुर्ग वहां पहुंचे. कपड़ो से और चेहरे से वे काफी अमीर लग रहे थे.

बुजुर्ग ने चिंता का कारण पूछा तो उसने अपनी सारी कहानी बता दी.

बुजुर्ग बोले -” चिंता मत करो. मेरा नाम John D. Rockefeller है.

मैं तुम्हे नहीं जानता,पर तुम मुझे सच्चे और ईमानदार लग रहे हो. इसलिए मैं तुम्हे दस लाख डॉलर का कर्ज देने को तैयार हूँ.”

फिर जेब से checkbook निकाल कर उन्होंने रकम दर्ज की और उस व्यक्ति को देते हुए बोले, “नौजवान, आज से ठीक एक साल बाद हम ठीक इसी जगह मिलेंगे. तब तुम मेरा कर्ज चुका देना.”

इतना कहकर वो चले गए.

युवक shocked था. Rockefeller

तब america के सबसे अमीर व्यक्तियों में से एक थे.

युवक को तो भरोसा ही नहीं हो रहा था की उसकी लगभग सारी मुश्किल हल हो गयी.

उसके पैरो को पंख लग गये.

घर पहुंचकर वह अपने कर्जो का हिसाब लगाने लगा.

बीसवी सदी की शुरुआत में 10 लाख डॉलर बहुत बड़ी धनराशि होती थी और आज भी है.

अचानक उसके मन में ख्याल आया. उसने सोचा एक अपरिचित व्यक्ति ने मुझपे भरोसा किया,

पर मैं खुद पर भरोसा नहीं कर रहा हूँ.

यह ख्याल आते ही उसने चेक को संभाल कर रख लिया.

उसने निश्चय कर लिया की पहले वह अपनी तरफ से पूरी कोशिश करेगा,

पूरी मेहनत करेगा की इस मुश्किल से

निकल जाए. उसके बाद भी अगर कोई चारा न बचे तो वो check use करेगा.

उस दिन के बाद युवक ने खुद को झोंक दिया.

बस एक ही धुन थी,

किसी तरह सारे कर्ज चुकाकर अपनी प्रतिष्ठा को फिर से पाना हैं.

उसकी कोशिशे रंग लाने लगी. कारोबार उबरने लगा, कर्ज चुकने लगा. साल भर बाद तो वो पहले से भी अच्छी स्तिथि में था.

निर्धारित दिन ठीक समय वह बगीचे में पहुँच गया.

वह चेक लेकर Rockefeller की राह देख रहा था

की वे दूर से आते दिखे.

जब वे पास पहुंचे तो युवक ने बड़ी श्रद्धा से उनका अभिवादन किया.

उनकी ओर चेक बढाकर उसने कुछ कहने के लिए मुंह खोल ही था की एक नर्स भागते हुए आई

और

झपट्टा मरकर वृद्ध को पकड़ लिया.

युवक हैरान रह गया.

नर्स बोली, “यह पागल बार बार पागलखाने से भाग जाता हैं

और

लोगो को जॉन डी . Rockefeller के रूप में check बाँटता फिरता हैं. ”

अब वह युवक पहले से भी ज्यादा हैरान रह गया.

जिस check के बल पर उसने अपना पूरा डूबता कारोबार फिर से खड़ा किया,वह

फर्जी था.

पर यह बात जरुर साबित हुई की वास्तविक जीत हमारे इरादे , हौंसले और प्रयास में ही होती हैं.

हम सभी यदि खुद पर विश्वास रखे तो यक़ीनन

किसी भी असुविधा से, situation से निपट सकते है.

” हमेशा हँसते रहिये,

एक दिन ज़िंदगी भी

आपको परेशान

करते करते थक जाएगी ।”

Think Beyond Infinity…

10:18 PM

+91 99 29 097300Prakash Sharma

[7/23/2015, 10:47 PM] +91 99 29 097300: Pl watch this video…. Without fail. I m sure that u ll never complaint about anything in ur life

10:47 PM

+91 99 29 097300Prakash Sharma

0:54

10:48 PM

+91 78 27 037060 CA Raghav Garg

[7/23/2015, 10:49 PM] +91 78 27 037060: जो डूबे है “शिव” की मस्ती में,

चार चांद लग जाते हें उनकी हस्ती में ।

……जय महांकाल…..

Jai baba Bhuteshwar

10:49 PM

+91 99 29 097300Prakash Sharma

2:06

11:00 PM

TODAY

CA Akhilender Singh

8:38 AM

CA Akhilender Singh

8:38 AM

+91 99 29 097300Prakash Sharma

1:48

9:12 AM

+91 99 29 097300Prakash Sharma

2:16

9:15 AM

+91 98 10 015863Vikas

[7/24/2015, 9:58 AM] +91 98 10 015863: एक डायलॉग बचपन से सुनते आ रहे हैं…

“अपने आप को पुलिस के हवाले कर दो”,

ये पहली बार सुन रहे हैं की एक…… बोल रहा है

“पुलिस को मेरे हवाले कर दो!”

केजरीवाल

9:58 AM

+91 98 10 636750CA M K Arora

[7/24/2015, 9:59 AM] +91 98 10 636750: भारतीय माता-पिता का सबसे प्रिय डायलाग …..

दिमाग तो बहुत है इसका,

बस पढाई पे ध्यान नहीं देता … !!

9:59 AM

CA Akhilender Singh

[7/24/2015, 10:01 AM] CA Akhilender Singh:

10:01 AM

+91 98 11 410304CA. Vipul Kapoor, C. A.

[7/24/2015, 10:05 AM] +91 98 11 410304:

10:05 AM

+91 98 10 156292Amit Bansal

[7/24/2015, 10:28 AM] +91 98 10 156292: संता: सर जी, आप

अपनी पत्नी को पार्टी में

क्यों नहीं लाते?

बॉस: वो गाँव की है!

संता: माफ़ करना, मुझे

लगा वो सिर्फ आपकी है!””

badtameez dil

10:28 AM

+91 98 10 156292Amit Bansal

10:29 AM

[7/24/2015, 12:25 PM] +91 88 00 224502: मैंने आज चेहरे के एक तरफ Dove लगाया

औr

एक तरफ मम्मी ने Mere कान के नीचे लगाया |

कान के नीचे लगायी हुई side ज्यादा चमक रही हैं |

Love u mom

12:25 PM

+91 98 99 709954sanjay sharma

5:29 PM

+91 98 68 655891CA. Dilip singh

[7/24/2015, 7:17 PM] +91 98 68 655891: आधार कार्ड के बंद आफिस के बाहर

लोगों की भीड़

लगी थी।

एक आदमी बार-बार आगे जाने

की कोशिश

करता और लोग उसे पकड़ कर पीछे

खींच लेते।

5-6 बार पीछे खींचे जाने के बाद

वह चिल्लाया:

‘लगे रहो लाइन में सालों, मैं आज

आॅफिस

ही नहीं खोलूंगा!’….

7:17 PM

[7/24/2015, 7:53 PM] +91 88 00 224502: Query: How to calculate LTCG

Year 2010

Flat booking (Own fund) Rs. 12,16,015

Bank Loan Rs. 30,00,000

2014

Sale before possession

Sale consideration: Rs.60,00,000

Transfer Charges Rs 2,00,000

Bank Loan Repayment Outsatnding : Rs. 21,00,000

Interest paid from 2010 to 2014 Rs.9,94,412

How to calculate LTCG

7:53 PM

YESTERDAY

CA Akhilender Singh

7:28 AM

+91 99 90 057390CA Atul Agrawal

[7/23/2015, 9:56 PM] +91 99 90 057390: CIC directs bank to provide information as to under what regulations loan applicants are required to get their project reports certified by CA

Central Information Commission New Delhi vide order dated 19-06-2015 has directed Central Public Information Officer(CPIO),Bank of India to forward to the Appellant a certified copy of the bank regulations / guidelines, which require loan applicants to submit their project reports and project balance sheets certified by a Chartered Accountant.

In case there are no such specific regulations / guidelines, the CPIO should inform the Appellant accordingly in writing. The CPIO to comply with above directives within fifteen days of the receipt of order, under intimation to the Central Information Commission

9:56 PM

+91 78 27 037060 CA Raghav Garg

[7/23/2015, 9:59 PM] +91 78 27 037060:

9:59 PM

+91 98 10 502399CA.Manoj Sangal

[7/23/2015, 10:18 PM] +91 98 10 502399: Nice Story

अमेरिका की बात हैं. एक युवक को व्यापार में बहुत नुकसान उठाना पड़ा.

उसपर बहुत कर्ज चढ़ गया, तमाम जमीन जायदाद गिरवी रखना पड़ी . दोस्तों ने भी मुंह फेर लिया,

जाहिर हैं वह बहुत हताश था. कही से कोई राह नहीं सूझ रही थी.

आशा की कोई किरण दिखाई न देती थी.

एक दिन वह एक park में बैठा अपनी परिस्थितियो पर चिंता कर रहा था.

तभी एक बुजुर्ग वहां पहुंचे. कपड़ो से और चेहरे से वे काफी अमीर लग रहे थे.

बुजुर्ग ने चिंता का कारण पूछा तो उसने अपनी सारी कहानी बता दी.

बुजुर्ग बोले -” चिंता मत करो. मेरा नाम John D. Rockefeller है.

मैं तुम्हे नहीं जानता,पर तुम मुझे सच्चे और ईमानदार लग रहे हो. इसलिए मैं तुम्हे दस लाख डॉलर का कर्ज देने को तैयार हूँ.”

फिर जेब से checkbook निकाल कर उन्होंने रकम दर्ज की और उस व्यक्ति को देते हुए बोले, “नौजवान, आज से ठीक एक साल बाद हम ठीक इसी जगह मिलेंगे. तब तुम मेरा कर्ज चुका देना.”

इतना कहकर वो चले गए.

युवक shocked था. Rockefeller

तब america के सबसे अमीर व्यक्तियों में से एक थे.

युवक को तो भरोसा ही नहीं हो रहा था की उसकी लगभग सारी मुश्किल हल हो गयी.

उसके पैरो को पंख लग गये.

घर पहुंचकर वह अपने कर्जो का हिसाब लगाने लगा.

बीसवी सदी की शुरुआत में 10 लाख डॉलर बहुत बड़ी धनराशि होती थी और आज भी है.

अचानक उसके मन में ख्याल आया. उसने सोचा एक अपरिचित व्यक्ति ने मुझपे भरोसा किया,

पर मैं खुद पर भरोसा नहीं कर रहा हूँ.

यह ख्याल आते ही उसने चेक को संभाल कर रख लिया.

उसने निश्चय कर लिया की पहले वह अपनी तरफ से पूरी कोशिश करेगा,

पूरी मेहनत करेगा की इस मुश्किल से

निकल जाए. उसके बाद भी अगर कोई चारा न बचे तो वो check use करेगा.

उस दिन के बाद युवक ने खुद को झोंक दिया.

बस एक ही धुन थी,

किसी तरह सारे कर्ज चुकाकर अपनी प्रतिष्ठा को फिर से पाना हैं.

उसकी कोशिशे रंग लाने लगी. कारोबार उबरने लगा, कर्ज चुकने लगा. साल भर बाद तो वो पहले से भी अच्छी स्तिथि में था.

निर्धारित दिन ठीक समय वह बगीचे में पहुँच गया.

वह चेक लेकर Rockefeller की राह देख रहा था

की वे दूर से आते दिखे.

जब वे पास पहुंचे तो युवक ने बड़ी श्रद्धा से उनका अभिवादन किया.

उनकी ओर चेक बढाकर उसने कुछ कहने के लिए मुंह खोल ही था की एक नर्स भागते हुए आई

और

झपट्टा मरकर वृद्ध को पकड़ लिया.

युवक हैरान रह गया.

नर्स बोली, “यह पागल बार बार पागलखाने से भाग जाता हैं

और

लोगो को जॉन डी . Rockefeller के रूप में check बाँटता फिरता हैं. ”

अब वह युवक पहले से भी ज्यादा हैरान रह गया.

जिस check के बल पर उसने अपना पूरा डूबता कारोबार फिर से खड़ा किया,वह

फर्जी था.

पर यह बात जरुर साबित हुई की वास्तविक जीत हमारे इरादे , हौंसले और प्रयास में ही होती हैं.

हम सभी यदि खुद पर विश्वास रखे तो यक़ीनन

किसी भी असुविधा से, situation से निपट सकते है.

” हमेशा हँसते रहिये,

एक दिन ज़िंदगी भी

आपको परेशान

करते करते थक जाएगी ।”

Think Beyond Infinity…

10:18 PM

+91 99 29 097300Prakash Sharma

[7/23/2015, 10:47 PM] +91 99 29 097300: Pl watch this video…. Without fail. I m sure that u ll never complaint about anything in ur life

10:47 PM

+91 99 29 097300Prakash Sharma

0:54

10:48 PM

+91 78 27 037060 CA Raghav Garg

[7/23/2015, 10:49 PM] +91 78 27 037060: जो डूबे है “शिव” की मस्ती में,

चार चांद लग जाते हें उनकी हस्ती में ।

……जय महांकाल…..

Jai baba Bhuteshwar

10:49 PM

+91 99 29 097300Prakash Sharma

2:06

11:00 PM

TODAY

CA Akhilender Singh

8:38 AM

CA Akhilender Singh

8:38 AM

+91 99 29 097300Prakash Sharma

1:48

9:12 AM

+91 99 29 097300Prakash Sharma

2:16

9:15 AM

+91 98 10 015863Vikas

[7/24/2015, 9:58 AM] +91 98 10 015863: एक डायलॉग बचपन से सुनते आ रहे हैं…

“अपने आप को पुलिस के हवाले कर दो”,

ये पहली बार सुन रहे हैं की एक…… बोल रहा है

“पुलिस को मेरे हवाले कर दो!”

केजरीवाल

9:58 AM

+91 98 10 636750CA M K Arora

[7/24/2015, 9:59 AM] +91 98 10 636750: भारतीय माता-पिता का सबसे प्रिय डायलाग …..

दिमाग तो बहुत है इसका,

बस पढाई पे ध्यान नहीं देता … !!

9:59 AM

CA Akhilender Singh

[7/24/2015, 10:01 AM] CA Akhilender Singh:

10:01 AM

+91 98 11 410304CA. Vipul Kapoor, C. A.

[7/24/2015, 10:05 AM] +91 98 11 410304:

10:05 AM

+91 98 10 156292Amit Bansal

[7/24/2015, 10:28 AM] +91 98 10 156292: संता: सर जी, आप

अपनी पत्नी को पार्टी में

क्यों नहीं लाते?

बॉस: वो गाँव की है!

संता: माफ़ करना, मुझे

लगा वो सिर्फ आपकी है!””

badtameez dil

10:28 AM

+91 98 10 156292Amit Bansal

10:29 AM

[7/24/2015, 12:25 PM] +91 88 00 224502: मैंने आज चेहरे के एक तरफ Dove लगाया

औr

एक तरफ मम्मी ने Mere कान के नीचे लगाया |

कान के नीचे लगायी हुई side ज्यादा चमक रही हैं |

Love u mom

12:25 PM

+91 98 99 709954sanjay sharma

5:29 PM

+91 98 68 655891CA. Dilip singh

[7/24/2015, 7:17 PM] +91 98 68 655891: आधार कार्ड के बंद आफिस के बाहर

लोगों की भीड़

लगी थी।

एक आदमी बार-बार आगे जाने

की कोशिश

करता और लोग उसे पकड़ कर पीछे

खींच लेते।

5-6 बार पीछे खींचे जाने के बाद

वह चिल्लाया:

‘लगे रहो लाइन में सालों, मैं आज

आॅफिस

ही नहीं खोलूंगा!’….

7:17 PM

[7/24/2015, 7:53 PM] +91 88 00 224502: Query: How to calculate LTCG

Year 2010

Flat booking (Own fund) Rs. 12,16,015

Bank Loan Rs. 30,00,000

2014

Sale before possession

Sale consideration: Rs.60,00,000

Transfer Charges Rs 2,00,000

Bank Loan Repayment Outsatnding : Rs. 21,00,000

Interest paid from 2010 to 2014 Rs.9,94,412

How to calculate LTCG

7:53 PM

pls ignore

Query: How to calculate LTCG

Year 2010

Flat booking (Own fund) Rs. 12,16,015

Bank Loan Rs. 30,00,000

2014

Sale before possession

Sale consideration: Rs.60,00,000

Transfer Charges Rs 2,00,000

Bank Loan Repayment Outsatnding : Rs. 21,00,000

Interest paid from 2010 to 2014 Rs.9,94,412

How to calculate LTCG

Personalized consultation is available on paid basis.

At the time

of sale of residential property if agreed

value is more than Rs. 50 lakhs than 1% TDS is deducted by the buyer out of

sale value. Please advise long term capital gain is to be calculated on the net

amount received after 1% Tax Deducted at

source (TDS) by the buyer or on agreed

sale value.

Capital Gain will be on total sale value.

Dear Sir,

Suppose one buys a flat for Rs. 20 lac and pays 2 lac as bank interest. Next year he has to sell the flat at Rs. 22 lac. Under this case shouldn’t STCG be zero considering the interest paid to bank as cost of acquisition. I am not able to understand the logic why interest amount paid to bank is not included into cost of acquisition. Thanks

Interest is not included in cost of acquisition. STCG will be 2 lac.

For Surcharge calculation in ITR does the Income and Capital Gain get clubbed. Example Income less than 1000000. LTCG 9900000. Total exceeds 10900000. Is surcharge payable. If yes then can some amount be deposited in PSB CGDeposit Account for 2 or 3 years and show the LTCG in that relevant FY

Surcharge will be applicable. Capital Gain account is better idea.

Thank You

Dear Sir,

Capital gain is computed by deducting the cost of acquisition, cost of improvement and any expenditure incurred in connection with transfer from the sale consideration. Kindly advise me :

1. Can Stamp paper duty and Registration fee be included in Cost of acquisition?

2. Is Broker’s commission deductible from sale consideration?

3. Can 1% TDS be deducted from Capital gains to arrive at net long term Capital Gain to

be deposited in LTCG account in Bank?

1. Yes

2. Yes provided you have payment receipt

3. Yes

Please advice as i had sole property in June 2015 of which had gained

capital gain of Rs. 13 lacs and wherein had invested into Capital Gain

account in corporation bank in July 2015, and the proerty which

investing is under construction and the project will be

completed/possession in 2018 or 2019 and from capital gain can i pay the

whole Rs. 13 lacs to builder and still can save tax as property

possession is after 36 months. Please advice

You can claim capital gain exemption u/s 54F of the income tax act.

Thank you sir for kind reply, appreciate the same

Hi

I work for an MNC which has given company stocks in 2010-11 FY which are NASDAQ studies held in US stock holding account (Schwab). The value of this stocks is calculate in Indian currency at average monthly stock value at averaged FX rate of that month. This is taxed as part of FY 2010-11 income. I have been submitting W-BEN form to my company to withheld tax. I sold these stocks in 2014-15. Question is “do I have to pay income tax for Indian government”?, Do I have to pay tax only on the gain or on the full amount of income given by my company? Does this gain get treated as long term capital gain? Will this amount be eligible for tax exemption under 54x rules like investment in house property or NHAI, REC bonds?

I need to check some more details to answer this query. This forum is only for general discussion. You may opt for advisory service on paid basis.

Hi Nitin,

This is Ajay.

We had purchased property on 29th March 2012 at 29 lacs

But registration is completed on 14th May, 2012

Now, we want to sell the property on 15th Oct, 2015

The Gain would be LTCG

I have following question:

1. Can you confirm my Cost Inflation Index Value of FY of Purchase?

a. Will it be 2011-12 i.e. 785?

b. Will it be 2012-13 i.e. 852?

2. The offer price is 39 lacs

a. Can I consider indexation and pay 20% of Capital Gain after indexation?

b. Can I avoid indexation and pay 10% on Net Gain(i.e. 39 lacs – 28 lacs = 11 lacs)

10% of 11 lacs = 1.1 lacs as Capital Gain Tax?

1. A

2. Option B is not available now. Only option is with indexation.

Hi Sir,

My Father bought a flat at Rs.1,83,000 in 1996. In 2011, he spent Rs.5,00,000 for renovation (Furniture Flooring, Coloring etc.) for the same flat. Now he sold flat at Rs.15,80,000.

What amount of tax is payable.

It require some other details and calculation. You may opt for personalized consultation.

pl inform me reply

Sir, please let me know the current Cost of Inflation Index for FY 2015-16.

1081

Sir i want to know when all do get the benefit of cost if acquisition?

If I plan to purchase a another property, do we need to invest the entire amount received as consideration or indexed cost of acquisition will be be deducted to calculate the amount to be invested?

Only capital gain

Sir.

I booked an under-construction apartment last year (2014). At that point, Builder sent me two different agreements – a sale agreement (that described the UDS) and a construction agreement, which roughly divided the total costs into two halves – land value and construction value.

Now, the apartment is closed to possession and builder is forcing me to do a sale deed just based on the sale agreement (which is based on UDS – roughly half of the total cost). I am not sure why the registration+stamp-duty charges are being calculated on land value (and not the total cost=landValue+constructionValue). Isn’t this illegal ?

I am asking this because if tomorrow I sell the property my cost of acquisition of the property will be shown as the one on the sale deed (which i guess will be the land value ?). This will increase my capital gains by a huge amount. Is there a way to include construction costs into my cost of acquisition or does it always have to be the sale deed value?

Thanks for your expert advise!

Its a normal practice to save stamp duty and registration charges. You will not face any problem in future.

Sir Can Long Term Capital gain be used to serve another on-going home loan?

No

Dear Sir,

I would like to have some clarifications of the below mentioned fact.

My father and mother have a joint property (flat) in the both of their name.

My father died few years back leaving my mother, my unwed sister and myself. My father has also left no will regarding the property.

Now, We would like to sell the property. I had talked to local lawyer in this regards. It is informed by him that I had also some percentage in the property on my father’s part (i.e . 1/3 rd of 50% of the property owned by my father). However, we have not changed anything in the mutation. Now if we have to sell the above captioned property:

1. How to Register all of our name i.e. my mother, sister and myself in the property before selling? please mention the detail procedures.

2. In this situation, without making any inclusion of all legal heirs, can the property be sold?

3. My mother and sister are not working and having PAN Card. In case of sale of the property, the capital gain raised and how the same will be distributed? like ownership in the property?

4. if so, then we have to file three separate IT Returns for total capital gain raised in percentage of ownership?

5. If after selling the property, a new property shall be bought jointly in the name of my mother and sister within 2 years of the sale, then how capital gain tax will be calculated?

In this case, my case will also be considered for capital gain tax?

1. You need to obtain succession certificate as per Hindu Succession Act and then you can transfer your father’s share in 3 parts i.e. 16.66% in your name, same share in your sister and mother’s name. After this, your mother will have 66.66% and you & your sister will have 16.66% each.

2. No

3. In the proportion of ownership as i explained in point no 1

4. Yes

5. It require complete calculation. I cannot comment without calculations. If you will not be part of new property then you need to pay capital gain tax.

thanks you a lot.

Myself NRI, want to sell ancestral plot (not house) and want to claim exemption u/s 54F. For claiming exemption, can I make use of booking of a residential flat made 2 years before (allotment letter from builder recd) but possession and sale deed execution shall be in about 1-2 year’s time. I don’t have any other residential property in India. Thanks in advance. Regards.

A property booked 2 years before the sale of existing property cannot be considered as a property investment to save capital gain.

Hhhjh

I hope all is well.

I wanted to seek your advice in regard to a property transaction.

On May 30, 2013 My Nani entered into a collaboration agreement with a builder whereby builder will demolish the current house having 3 floors and reconstruct 4 new floors and keep 1 floor with himself . As a part of agreement builder will take one floor and give cash of 60 Lakh to her (5 Lakh at time of agreement, 5 Lakh at the time of taking over the land for construction and remaining 50 Lakh at the time of executing the sale deed ). The builder paid initial 10 lakh in cash .Recently (Sep 4,2015 )the sale deed of 1 floor was executed between my nani and another party (not the builder ) whereby the sale deed is executed for Rs 56,80,000 . Builder has verbally said at the time of sale deed creation that he is giving the amount in excess of Rs 50,00,000 for lift however no where specifically in the sale deed this is stated.

The property plot was allotted on April 14, 1988 in consideration of Rs.11,800 . The conveyance deed was however executed on 8 Oct, 2001.

I would like to know whether there is any long term capital gain applicable on this transaction and how much ??

How can I save this tax liability ???

PS: my nani intends to give equal money to both her daughters which she has received as a result of this transaction.

Long term capital gain will be applicable. To calculate the same more details are required. The gift from mother to daughter will be tax free in hands of daughters.

Sir what is the tax rate for debentures.

And after how many month it wil become long term?

Interest is clubbed with income and taxed at marginal IT rate. Short term capital gain tax is applicable if you sell before 1 year. If you sell after 1 year but before maturity then long term capital gain tax is applicable. At maturity there is NO Capital gain tax applicable.

Hello Nitin Sir,

My Nana had bought a property almost 50yrs back in Thane. It’s now on My Moms and My Uncle’s name 50-50%. We are planning to sell it to builder at 1.4cr. Thereby my Mom will get approx 70L. Wil it incurr Long Term Capital Gain Tax to my Mom. If yes, how to save the same?

Long term capital gain is applicable on inherited property. Your mother can save either by investing in a new property or can buy Capital Gains Bond issued by REC and NHAI.

TY Sir.

I have a house which is on Loan currently.

If my Mom pays-off the loan, will that amount be Tax free under LTCG?

As you have deleted previous comment therefore i will not be able to answer your query. Its quite unprofessional on part of readers to delete the comment after the query is answered. My sincere apologies for same.

Hello Nitin,

My Mother would get around 60 L from ancestral property. I will have to invest them in new property or REC/NHAI.

My query is:

1. I have bought a house 2 months back with a loan of 30L. Can she repay my loan amt to bank and show that money as invested and exempt from LTCG?

l

2. If I purchase other flat in coming 2 years say for say 80L, how can I show that, among my 80L, 60L belongs to my Mother thereby exempting her from LTCG?

Investment suggestions if any, are welcome.

Thanks in advance.

sir my dad has purchased the a plot in 2001 of 1,31,366 and sold it in 2015 of 16,00,000. and spend the complete amount in my fees (10 lakh / year) and rest in car loan . what can be the ways to exempt from the tax .

Your father need to pay long term capital gain tax on the transaction. Unfortunately, you cannot save LTCG in this case.

Let us say, I sold some shares (stock-1) and holding period is less

than one year. I have used the complete sale proceeds to buy the

shares (stocks-2) again in the same financial year. Is the gain due to selling the stock-1

taxable?

In case of capital gain due to sale of the property, if it is

reinvested to buy another property becomes exempted from IT. Is it

same in case of stocks too or is it different?

Short term capital gain tax will be applicable. The provision to save STCG is not available for both the stocks and the property.

Hi Nitin,

Per the index table on your forum, I don’t seem to have any Capital Gain liability (Booked under construction property in 2006, Acquisition in 2011, Selling in 2015-16). Is there a way to get the No Tax Certificate on this basis and avoid the 20.66% TDS by the buyer of my property?

Regards,

Nitin

If the capital gain is NIL or capital loss then you can apply for NIL deduction certificate.

1. My father purchased a land in 1964 , area 4000 sft at patna, bihar.

2. He transferred the land to his two sons in 1995.

3. in 2012-13, we ( two brothers) asked a developer to build flat and give us 50%.

4. i got two flats and sold one flat in 2013-14

how should i calculate capital gain tax?

It is complex case and two step calculation. Without going through agreement with builder and other details it is difficult to comment. I suggest you to hire a local CA who can help in calculation.

i know sir. i already contacted few CA in Patna but no body gave clear picture. when i could not get it done i thought to contact experts on internet. can i derive CG = sale value – construction cost and pay short term capital gain. give some basic idea to arrive at CG. One of the CA is telling that i have to pay LTCG on land also. we gave builder right to enter and construct the building and hand over 50% flat. Builder has already sold his part of 50% and gone.

i shall appreciate if you throw some light to proceed.

It is inherited property therefore capital gain will be long term capital gain. You need to calculate separately for land and construction. Secondly, as i mentioned it will depend on your arrangement with the builder. Cost of construction can be included depending on the UDS you forego in lieu of payment from builder or barter deal with the builder.

sir, i understand , i am asking too much. just one more point-

1. land was in name of we two brothers as per will of father.

2. We did not give full right of the land to builder but only for necessary formalities and construct flat.

3. He developed 8 flats

4. He sold his 4 flats of his share. we had no role in that. so he used 50% of land in lieu of construction of all 8. We did not receive any money for the land either initially from builder nor from sale of builder portion.

5. my brother has no plan to sell his portion and as on today, he is not paying any tax on 2 flats he got.

6. I sold one flat and i have mentioned in the agreement , cost of construction and cost of land separately. clubbing them make Rs.56 lacs.

7. I thought , since land is inherited, there is no tax.

8. builder got right to construct flat and as compensation, he got 4 flats and he sold. it was not a sale..

9. since total area is 4000 sq. feet, do u mean i have to pay LTCG on the value of 2000 sft. ( will it be indexed value or market value?

10. do i have to pay LTCG on super built up are of flat? ( indexed or fair market value)?

11. can i calculate SHART TERM CAPITAL GAIN as : total sale value- cost of construction of the one flat i sold ? and pay tax.

As i mentioned, the queries can be answered only after going through all the details. This forum is only for general discussion. If you wish to avail personalized consultation on paid basis then request you to mail at info@Nitin Bhatia.in

My father purchased a property in 21/5/2010 worth of 283000

and he registered the property to me through sales deeds not through gift, in

sales deeds property value is written as 718000 on 30/4/2013. Income notice has

come regarding capital gain tax. Is there any way to prove that there is no

money transferred in this case and it’s been registered to son by father and if

so will it save the capital gain tax?

As it is sale deed therefore it cannot be proved that no money exchanged hands. Secondly, even if you prove somehow that it was gift then also capital gain tax is applicable. In my opinion, you should be pay capital gain tax as demanded by IT department.