Atal Pension Yojana was launched by Prime Minister of India Sh. Narendra Modi on May 09, 2015. This scheme was launched along with 2 other insurance schemes i.e. Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY). Atal Pension Yojana is a social security scheme. It is named after former Prime Minister of India Sh. Atal Bihari Vajpayee Ji. The scheme will be launched w.e.f 1st June, 2015. As usual, when i searched internet i found hundred of articles on Atal Pension Yojana which are simply cut, copy and paste of information available on official website. The objective of my post is to give the 360-degree perspective of social security scheme. Trust me you can find much more details on Govt of India’s website then what i or any other financial planners can share in 1000 words or so.

Why Atal Pension Yojana is Launched?

When i was going through deciding phase of my career, i remember there was a maddening craze for Govt Jobs. In fact, my both parents were Govt Servants. An individual with Govt job was most sought after Bride / Groom during those times. The only reason for this madness was Social Security attached to Govt Job. A Govt Servant was assured of Life Long Pension after he/she retires. In short, there was no concept of retirement planning at that time. My father was working at a very good position in one of the leading private companies in early 70’s. My Grand Father insisted him to join the Govt job at much lower salary. Considering his potential, i personally feel that he would have retired at a very senior position in the private job. The carrot of “Life Long Pension” was so compelling that he sacrificed his golden career for a Govt Job.

During those days due to low literacy level and being an agricultural country, demand for jobs in the service sector was low. In short, it was relatively easy to get a Govt job. Over a period of time, demand overtook supply but Govt was not able to generate enough jobs. Secondly, the pension payout of govt ballooned due to higher life expectancy ratio. To control the pension payout, Govt launched Defined Contribution Pension Scheme from Jan 01, 2004. Under this scheme, any govt servant joining govt services on or after this date will not get Life Long Pension from Govt. Both Govt and Govt employee will pool amount equivalent to 10% of Basic + DA of employee’s salary in Pension Account. This addressed the issue of rising pension bills.

The critical issue is related to Social Security, which was unanswered. As i mentioned in my post Make in India – Key to Revival of Economy that most of the jobs which will be generated under Make in India initiative will be for Low-Skilled / Unskilled workers. In short, the future job boom will be in unorganized sectors. Not many people will be willing to take a job in the unorganized sector until unless there are Financial Benefits & Social Security attached to it. Atal Pension Yojana is a step towards providing social security to workers in the unorganized sector.

Summary of Atal Pension Yojana in 25 points

1. A Pension Scheme for unorganized sector workers.

2. Min and Max age of entry under Atal Pension Yojana is 18 years and 40 years.

3. Pension will start at the age of 60 years.

4. Premature withdrawal is allowed only in case of a death of a beneficiary or terminal disease.

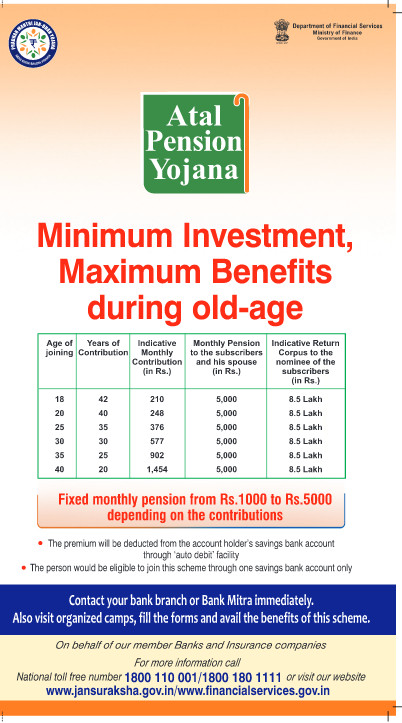

5. Depending on the contribution of a beneficiary, under Atal Pension Yojana there is a guaranteed pension of Rs 1,000 to Rs 5,000 per month in the multiples of 1000’s.

6. Monthly contribution to Atal Pension Yojana is allowed

7. In case of discontinuation of payment:

After 6 months, account will be frozen

After 1 years, account will be deactivated

After 2 years, account will be closed

8. The beneficiary should not be covered under statutory social security scheme of Govt of India.

9. The subscriber can opt for nomination facility.

10. Govt will contribute 50% of the total contribution or Rs 1000 per annum, whichever is lower to Atal Pension Yojana Accounts opened on or before 31st Dec, 2015. This contribution will be for 5 years from 2015-16 to 2019-20. The beneficiary should not be an income tax payer to avail Government co-contribution.

11. Registered beneficiaries of Swavalamban Yojana aged between 18 – 40 will be automatically migrated to Atal Pension Yojana with an option to exit.

12. An individual can open only 1 account under Atal Pension Yojana.

13. Official website of Atal Pension Yojana scheme is http://www.jansuraksha.gov.in/

14. You can call on following toll-free no’s to get scheme details

National Toll-Free – 1800-180-1111 / 1800-110-001

To know helpline no of your state, Click Here

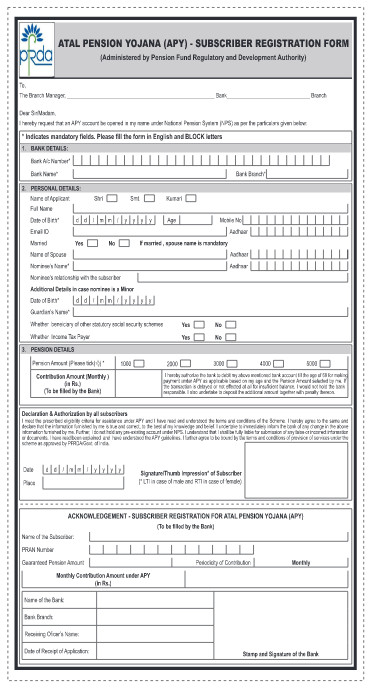

15. The forms of Atal Pension Yojana are available in 9 languages. To download the form, Click Here. Sample English form is as follows.

16. To open an account under Atal Pension Yojana, contact your bank and provide APY application form, Aadhaar number and mobile no.

17. If you don’t have a bank account then open the new bank account by submitting KYC documents, Mobile no and Aadhaar number along with application form of Atal Pension Yojana. You cannot opt for this scheme without bank account details.

18. You also need to provide authorization letter to set up auto debit facility and Spouse / Nominee details. The only mode of contribution to this scheme is through the auto debit facility from the bank account. Cash / Cheque / DD / Online Payment or any other mode of payment is not available as of now.

19. There is no tax deduction available on the contribution towards Atal Pension Yojana. Pension received will be taxable as an income from salary.

20. If you are an existing EPF account holder then you cannot opt for co-contribution from Govt’s end.

21. Aadhaar number is not mandatory to open an account under Atal Pension Yojana though it is desirable that it should be provided.

22. The beneficiary will receive SMS alerts related to account details/activity. He / She will also receive a physical statement at regular intervals.

23. On death of a beneficiary before attaining 60 years of age, the nominee will receive monthly pension and will also receive lump-sum amount depending on the pension amount

Monthly Pension of Rs 1000: 1.70 lakh

Monthly Pension of Rs 2000: 3.40 lakh

Monthly Pension of Rs 3000: 5.10 lakh

Monthly Pension of Rs 4000: 6.80 lakh

Monthly Pension of Rs 5000: 8.50 lakh

24. The monthly contribution can be changed once in a year for higher / lower pension amount.

25. There is no fixed due date for auto debit of the monthly contribution. Bank can recover the contribution any day during the month as and when the funds are available.

Few Concerns

1. Any social security scheme in India is prone to misuse. Though the government is creating a centralized database of all the beneficiaries under Atal Pension Yojana. If the misuse of this scheme is not controlled then it might be a nightmare to control the pension outflow or settle insurance claims. Best examples of misuses are MGNREGA or leakage of LPG subsidy (Which is fixed to a large extent). The probability of misuse is high as there is a lump sum payment on the death of a beneficiary & pension. Therefore, a person may enroll for all 3 new launched social security schemes to avail the benefits.

2. Inflation: Though a pension of Rs 5000 may sound decent today, but the scheme has not considered inflation adjustment. A pension of Rs 5000 after 20 years might not be sufficient to survive for few days due to inflationary pressures. An inbuilt mechanism should be there to adjust the contribution and pension amount to account impact of inflation.

3. Legal Disputes: As i observed that in most of the cases there is a dispute at the time of insurance claim settlement. As per the rule, the nominee is only the custodian of the insurance amount received. The amount is passed on to the either legal heirs of the deceased as per Succession Act or as per the WILL of the deceased. It may be an operational nightmare for banks to handle such cases under Atal Pension Yojana.

4. Rich Non-Tax Payers: Though scheme is for non-tax payers but what about non-tax payers like rich farmers or a rich businessman involved in small business activities. It will be sort of double bonanza for them. At a macro level, salaried class taxpayers are excluded from the Atal Pension Yojana.

You may post your queries/comments related to Atal Pension Yojana in following comments section.

Copyright © Nitin Bhatia. All Rights Reserved.

woww !!! thoroughly explained ,,kuos to @nitinbhatia121:disqus sir

Hi Nitin

Does this contribution falls in 80C exemptions.

Thanks

Tax deduction is not available on contribution towards APY.

sir,

I am a goverment employee and I am eligible for statutary pension after retirement.can I join this APY scheme.

You are eligible but will not get govt contribution.

Respected Sir i have just one quirey about Atal pension Yojana i have file INCOME TAX retrun in under Tax-Free Slab and i have not pay any tax to Income Tax Department than i’m eligible for Atal Pension Yojana Scheme

As you are not a tax payer therefore you are eligible for APY

Dear Sir, In Mumbai, Which bank (national, state level or co-operative) offer atal pension yojana scheme. 10 days befor i asked in abhudaya bank in parel for same scheme. but they told me we are not offering or they don’t no about this scheme, how it will work in future. and one thing is istallment of apy will increase by year by year? one uti bank officer told me, that increase by year by year as per age.

You may check with nationalized banks like SBI, Bank of Baroda, PNB etc. For other queries, please go through my post.

HI, I like your Blog.

As mention Swavlamban yojana can merge with APY. but I have open Tier 1 account under NPS

Swavalamban Yojana will merge with Atal Pension Yojana. You will be given an option to either to exit or migrate to APY.

agreed. But Swavlamban yojana and Tier 1 difference Instrument for pension.

Both are managed by NPS. that’s why I am asking both are merged or not.

Currently there is no clarity. You will receive communication regarding the same.

is EPF and PF same?

If you are an existing EPF account holder then you cannot opt for co-contribution from Govt’s end.

will i be able to enroll in this scheme Thank you

You can enroll but not eligible for co-contribution from Govt.

Thank you Sir

sir, I paid income tax for assessment yr-2014-15(fy2013-14). can I be eligiable for ‘Atal pension yojana’? pl. help me.

You are not eligible.

He is eligible.

If any one have PPF in post office saving scheme and endowment LIC plan is he/she eligible for Atal pension scheme.

I am assuming that you are not an income tax payer and also not covered under any social security scheme of Govt of India. In this case, you are eligible for Atal Pension Scheme.

Sir..my office deduct tax from salary and i posses Form 16 every year, but i have never file income tax returns. am i eligible for APY?

If you tax is deducted but you are not filing ITR then you may face penalty from IT department. You are not eligible for APY.

He is eligible for opening APY, but not for government co-ccontribution.

I am a Govt., employee my D/b-is 10/06/2015 can I apply for APY If I am eligible at present I am not tax payer after 2/3years may be I am tax payer then what is the conditions. If I am not eligible is it possible my wife can apply for the APY

Seems typo error. DOB mentioned in incorrect.

Sir, The beneficiary should not be an income tax payer. But what if in subsequent years income of beneficiary increases and became liable to pay income tax . Please clarify my above doubt

Very good query. Taxpayer condition is only at the time of opening account. In future, if you become tax payer then it will not impact existing scheme.

That would be a contradiction.

But taxpayers can join APY. No government co-contribution for them.

Income tax payer can join scheme, but they are not eligible to receive government co-ccontribution of upto Rs 1000 per year for 5 years.

sir,the age limit for adal pension yojana is 18-40 as per the notification.the dob of my husband is 22/05/1975 & he applied for apy.But the bank denied his application for apy,saying he is over age…i understood from the table given in site that in the age of 40 also v can join.kindly clarify

Your husband turned 40 years last month. For Govt schemes, if max age of entry is 40 years then it implies that till an individual turn 40 years. Therefore, in my opinion your husband is now not eligible for Atal Pension Yojana.

Hello Sir, please answer my queries.

1. I am 20 years young and i am a student. i want to avail APY scheme. i read the details. it says that i should not possess any other social security scheme. if i want to avail any other schemes any-day in future, will this cause problem at the time of receiving pension 40 years later?

2. suppose i end up having a govt. job in the coming years, and i start getting EPF, will the govt.’s contribution still be given as, when i availed the scheme i was not an employee ?

3. and if i become income tax liable in future, then ?

1. This condition is only at the time of subscription to scheme

2. There is no clarity on same

3. It will not impact your subscription to the scheme

i should go ahead with the scheme then. Thanks :)

Not true that tax payers are not eligible.

They are not eligible for the govermeny co-contribution of Rs 1000/- per year for 5 years.

That is what I understood.

No where it is mentioned that, tax payer can’t join APY.

But taxpayers are not eligible for government co-contribution.

Sir, I have a question. What if I stop or discontinue the scheme. Will i get the benefit of my investments then?

You will not get the benefits.

Hi Sir.. also can the spouse be the nominee ?

Yes

There is a column in a table as “Indicative Return Corpus to the nominee of the subscribers”… Does this mean this amount will be given to the nominee at the time of maturity (i.e. after 60 yrs ) in addition of the monthly pension ? Please brief if this is not the case.

This column means that if something happens to the subscriber before the maturity then this amount will be paid to the nominee besides pension.

sir i have submitted the atal pension yojna subscription form to the bank where i maintain savings account. they tried to register my account in this scheme but an error mesage is generated “subscribtion not valid”. the bank officials told me that you can’t register for this scheme although they are unable to tell me the exact reason. please could you tell me the reason? i am a student now, age 19.5 years and have no social statuitory scheme and no income tax. i have only LIC. please reply. thanking you, with regards – rahul

You can submit written complaint with the bank and wait for reply. I don’t foresee any reason.

Sir, have enrolled this scheme by last week only

and can i change the contribution amount

You can change contribution once in a year. Now you can change next year.

Good Evening Sir ! Sir I am private Employee. I do not pay income tax. But in future I may pay tax. I do not have any kind of pension scheme and I do not have PF scheme. Sir more recently I enrolled myself with NPS(Not Swawlamban) . I have NPS account Tier 1 and I have got PRAN Number. Now Am I elligible for Atal Pension Youjna ? Will I get government contribution in APY? What is the difference between NPS and APY ?

Swavalamban Yojana will merge with Atal Pension Yojana. You will be given an option to either to exit or migrate to APY.

Sir i want to cancel my Atal Pension yojana account due to some reason. Please tell me the procedure.

Please reply.

Thank you.

Rahul Baroi.

It cannot be cancelled. On non payment account will be closed.

one of my relative activate this scheme in two different bank accounts. so what he suppose to do to cancel this scheme in one account. is there is any option to contact to bank and remove the auto debit facility?

one of my relative activate this scheme in two different bank accounts. He also get 2 diferent PRAN Numbers. so what he suppose to do to cancel this scheme in one account. is there is any option to contact to bank and remove the auto debit facility?

Ideally bank will find out else you may submit written application with bank to discontinue one account.

if I need to close my Atal Pension plan, then what will I have to do as because SBI bank employee not able to help me for the same.

You may stop payment. After 2 years it will be closed.

the amount getting automatically debited monthly, so if I stop keeping money in bank my account will get stopped.

Yes or you can close the account.

whether NRI people are eligible for this Atal Pension plan..

No

You answered that NRI people are not eligible to join in Atal Pension Yojana. Would you please explain whehter a person who is working In UAE having NRI Saving account with SBI can join in Atal Pension Yojana. If your answer is ‘NO’, then how the SBI bank accepted his application ?

Normally banks don’t check the residency status.

I have paid a tax for financial year 2014-2015 ( assessment yr 2015-2016). I also filled a ITR. But currently I have no source of income. So can I apply for atal pension yojana? Will I get the government contribution?

You can apply for atal pension yojana but i don’t think so that you will get Govt contribution.

Does the nominee will get the corpus amount after death of both the subscriber & spouse while subscriber already crossed 60yrs of his/her age and both the subscriber & spouse already availed the pension for few years(say 10-15yrs) before their death.

It depends and also on respective succession law.

HI .. I am a tax payer and i work for a private company. So can I apply for Atal Pension Yojana? Will I get the government contribution?

You may apply for Atal Pension Yojana but will not be eligible for govt contribution.

will the lump sum amount be recovered even after we survive for 60 years, or it is payable only in case of death of the account holder?????

On survival only pension will be paid. It is annuity plan.

how to check balance of pension? how much amt i contributed till now?

Your bank can share this information.

I enrolled this scheme through SBI. Amount deducted my account automatically every month but do not give any statement. I already discuss about Banking staff but they told this is not their responsibility to give statement. Any suggestion- How I got statement ?

You will receive physical statements at specific intervals i.e. annually. Please wait for completion of 1 year to receive a statement.

when i enrolled into APY scheme in august 2015 i was just a student, no regular source of income, no taxpayer and was also not covered under any statutory social security scheme. But from feb 2016 i will have a proper salaried job , i will become a tax payer and i will also have a provident fund account so what will be my future under this scheme. Will I still be eligible under this scheme or not?

You are eligible and can continue your contribution to APY.

I am an government employee and I pay income tax. I have pran and contribute to CPF as mandatory for government employees who have joined after 2014. Can I also avail apy?

What are the statutory social security schemes? Where can I get the list?

I think PRAN no referred by you is issued under NPS. In my opinion, you are eligible for APY but you are not eligible for the govt contribution on this account. Please click on following link for social security schemes

http://www.jansuraksha.gov.in/

Dear Sir – Is it fine to open separate APY accounts for myself and my wife and keep my son and daughter as the nominees respectively?

You can do that depending on your financial requirement.

Sir, I am an government employee and I pay income tax. I have already PRAN under NPS mandatory for government employees who have joined

after 2004. Also i have opened the APY online from SBI Internet banking and received another PRAN number. Also i mentioned in the form that i am not a beneficiary of other social security schemes but i pay income tax.

It is not clear what is your query..Please mention.

Dear Sir,

I am Ramanathan. Working in private software organisation. 4 months before i joined in APY scheme in canara bank. i am not tax payer. my salary is 312000 per month. In future my salary will increase and i’ll pay tax. Now what is position of my APY scheme. Is i want to continue or discontinue? Please suggest me sir. I confused very much.

As you mentioned your salary is 3.12L/month therefore in my opinion you may discontinue APY.

Sir, I m in Private Job and contributing to EPF and also paying Income Tax, I have applied for Atal pension Yojna and my first prem Rs. 1196/- deducted from my account. Now, Please tell me whether I eligible for govt. contribution or not and also please suggest, Should I continue this or not.

You are not eligible for govt contribution. To continue/discontinue is your personal decision.

I’m salaried person and paying tax on my salary. M I elgibile for APY?? because it states that a person should be a non-Tax payer..

You are not eligible for Atal Pension Yojana.